1 Stock I Wouldn’t Touch With a 10-Foot Pole, Even After the Market Sell-Off Dropped Its Price

Even though Apple (NASDAQ: AAPL) stock dipped during last week’s sell-off to nearly 12% off its 2024 high (at Tuesday’s close), that wasn’t enough to make me want to buy it.

So why am I sour on a stock that so many others are bullish on? It all has to do with valuation.

Apple’s growth has been poor

If you live in the U.S., chances are you either own an iPhone or other Apple product, or know someone who does. Apple is a little less dominant worldwide, but is still a highly recognizable and popular brand.

Because Apple’s business is mostly centered on high-end electronics, it’s more prone to demand cycles than companies selling less expensive electronics. As inflation has taken its toll, Apple’s sales have struggled.

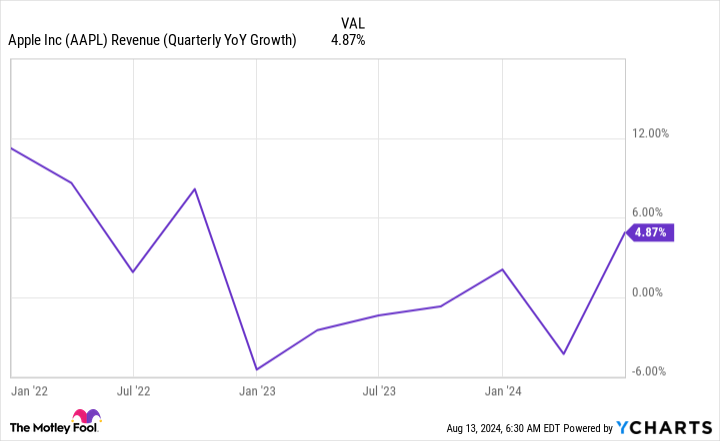

Since the start of 2022, Apple has struggled to post double-digit revenue growth and even had a few quarters where sales dipped compared to the year-ago period. Its latest quarter saw revenue increase year over year, but sales of its flagship product, the iPhone, decreased slightly year over year.

The last two and a half years would have been much worse for Apple if it weren’t for its services division. This encompasses revenue from advertising, the App Store, cloud services, and digital content like Apple TV and Apple Music. Unlike its hardware revenue, which fluctuates, services has more of a subscription-model feel to it, which is great to balance out the more cyclical side of the business.

But is that enough to justify purchasing the stock?

The numbers don’t add up for the stock

Premium companies trade for premium valuations. Some companies just have such high execution that investors are willing to pay up for them. Apple has been in this position for a while, but I’d like to challenge that notion.

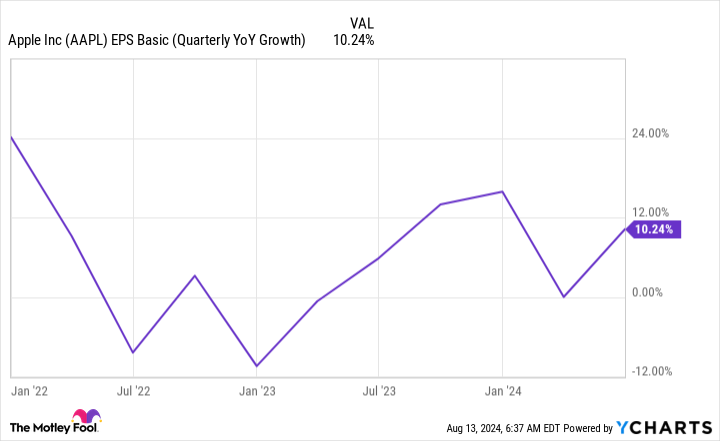

Its revenue growth has been poor, and while its earnings growth has somewhat kept up with the general market, it still struggles to post double-digit increases.

With Apple approaching three years of uninspiring results, I’m confident it doesn’t deserve its premium.

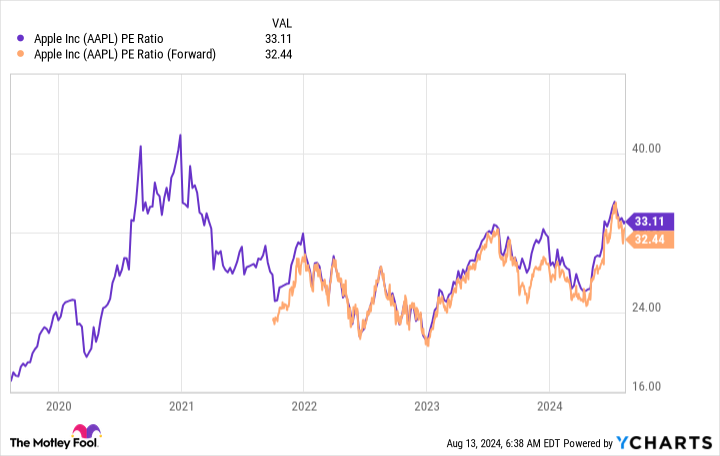

At 32 times forward earnings estimates and 33 times trailing earnings, the stock is as expensive as it was in early 2021. At that time, revenue was increasing by 50%, with earnings doubling year over year. Apple was worth the premium investors paid then, but the current Apple is not.

Its investors are holding on to the idea that Apple Intelligence, the company’s generative AI product, will be a must-have and cause consumers to upgrade to the latest iPhone. Because this feature can only be run on the latest generation of phones, it could cause an upgrade wave. But that’s not guaranteed and wouldn’t do much for the stock besides a one-time wave of demand.

There are much better tech investments. Microsoft trades at almost the same valuation yet has consistently posted double-digit revenue and earnings growth. Or you could look at Meta Platforms, which is cheaper and growing incredibly quickly (increasing revenue by 22% in the second quarter and earnings by 75%).

Apple is just too expensive and not performing as well as it needs to to justify its valuation. At these prices, there are far too many better companies to invest in, and I think investors should put their money there instead.

Should you invest $1,000 in Apple right now?

Before you buy stock in Apple, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Apple wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $763,374!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Meta Platforms. The Motley Fool has positions in and recommends Apple, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

1 Stock I Wouldn’t Touch With a 10-Foot Pole, Even After the Market Sell-Off Dropped Its Price was originally published by The Motley Fool

Source link